It’s tough scaling a private company. Organic growth can take decades to achieve critical mass. Say you get to $5m in sales and you can produce a compound annual growth of 10%. It takes 10 years to get to $13m. Is $13m critical mass in an industry? Probably not, although that would be a fair sized insurance broker, or a software company but you’d still be a small private company (in terms of biggest players in your sector).

Look at scaling this way. How rare is it for a private company to reach 100 employees? Very.

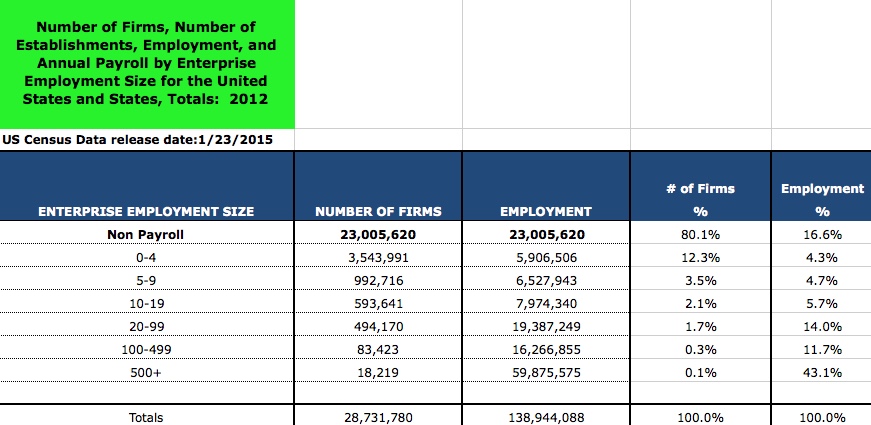

To be precise from the table below, you could conclude that only 0.4% of US entrepreneurial activity gets there – that’s 101,642 firms out of 28 million enterprises. Sorry if that was a shock.

Let me add to the debate further by adding the desire to exit your scaled business one day. Actually turn it into post tax cash in your bank account. Here’s another shocking statistic. The number of exits in the US each year that crystalize $10m or more pre-tax is around 6000 companies. Now you can do the math but if you join the dots, you can see how tough it is to scale to critical mass, and then how rare it is, to actually exit, you see can see that staying small might be risky. I mean risky in the sense of creating a retirement fund that doesn’t rely on you driving your business forever.

It’s my judgment that most small to medium enterprises producing less than $3m EBITDA are concerned about making payroll at least one quarter each year. Scale does deliver benefits. There’s just a minimum profit generation that’s safe. There’s a certain critical mass that gives you a predictability of sales, an alignment of resources, an ability to control your destiny and therefore a feeling of relative safety.

That’s the landscape that should force you to consider getting bigger by merging with a competitor or an appropriate complimentary business. In the limited space of a blog post, I’m going to leave you with some early questions to consider that will make the assessment and potential deal easier.

Checklist of Questions

- What does the merger create from a positioning point of view? Can you add significant greater value to your customers? Does the merger allow you to produce better outcomes for your customers? What’s the story on the new website going to be?

- Is there any chance of losing customers?

- Are the strengths and weaknesses of each side complimentary? Or are you just making a problem child bigger?

- Can you imagine a post-merger management structure? Rarely do joint CEOs work? Post-merger thinking needs to be done early and in far greater detail than you can ever imagine. Is it possible to produce a post-merger financial plan? Mimic the new entity in all its glory, financially, technically, and of course from an organization structure point of you.

- Be honest when you consider the culture of both enterprises. Will they play well in the sand?

- Valuation is clearly a huge hurdle to climb? The solution can be relatively simple. Remember it’s not so much the absolute $ valuation that matters but more the relative value. If you can agree that each shareholder camp will own 50% of the new entity, the headline deal is done! If not, you could agree to appoint an independent valuation firm who do these valuations every day (see DCF). In this case you agree to accept the relative values within reason. Or you appoint an acquisition adviser and take the lead as the acquirer to achieve a fair structure for Newco, the merged vehicle that reflects relative values.

- Delicate as it is, you need to address salaries and bonus structures across the whole company. Is there a problem? You will need to sell this deal to all staff not just senior management.

- Do both sets of shareholders want the same thing? Do they both want an exit in five years, ten years? How will you enforce this?

- What conditions need to be built into the shareholder agreement?

- Are there cost savings to be secured through procurement, excess resources, property consolidation, and other excess assets?

- Is the merger an opportunity to revisit the long-term structure of the balance sheet? Perhaps there’s an opportunity to bring in external equity capital. Perhaps there’s an opportunity to renegotiate banking terms, rates and guarantees.

I’ve framed the benefits of a merger in very simple, critical mass related benefits to increase shareholder value, to create safety and increase the probability of building a business that is saleable. However a merger can lead to real operational granular value that’s difficult to achieve by going it alone:

Benefits

- A deeper reservoir of great talent.

- Attract new talent from the marketplace because your story has become more compelling.

- Spreading R&D and new product investments across a broader base.

- A higher market share brings higher profits in most industries.

- Larger companies achieve higher exit multiples than small companies with similar growth trajectories in the same sector.

- The ability to pitch for bigger deals.

- As mentioned above, mergers can allow the participants to offer far stronger products or services to their customers.

Finally unlike many large public companies, I believe most private company owners have empathy for the bravery, selflessness and grit that their fellow owners have demonstrated to achieve their success to date. This will be vital to secure a fair and reasonable deal.

The Portfolio Partnership offers operational expertise to scale your business organically or by acquisition. We continue to transform visions into remarkable businesses.

Further reading: Why Private companies make great acquirers.