Valuation models are useless unless they are buyer specific!

Let’s look at the ingredients of most CPA type valuation models.

- Discussions with management regarding the history and future of the company.

- Historical financials and future projections of Profits and Cash including management presentations, business plans, and Shareholder Agreements.

- Balance Sheet Net Assets.

- Public company values and the Price Earnings ratios implied by that value.

- Previous transactions and the values paid.

- Economic outlook of your sector.

- Discounts related to lack of marketability of the shares (can’t trade on a stock market).

This generates a valuation based on

- A multiple of profits

- A multiple of Revenue

- The Net Assets

- An estimate of Net Present Value of future free cash flows (operating cash generated after Capex before funding costs)

Certainly logical. But here is the problem and why the “buyer specific” part is so important.

When several software acquirers are assessing your Boston based technology business, each acquirer is standing in their own shoes, their own location with their own portfolio of products, sales channels, org chart, IP, customer base, sector concentration.

Each acquirer, whether based in Tokyo, Paris, London or New York has a different strategic rationale for acquiring and integrating you. Each acquirer may have a different integration plan.

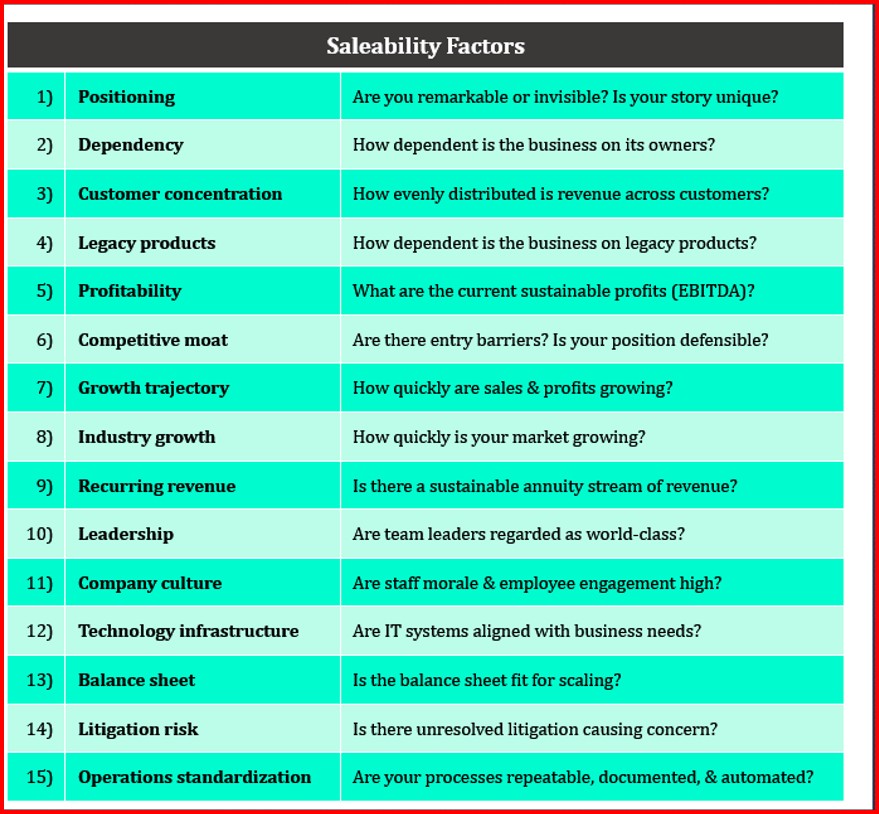

If they are practiced acquirers, they are likely to assess you using criteria in our Saleability Test:

So, each acquirer will assess your PERCEIVED VALUE to them, based on their strategic rationale, the criteria above and their integration strategy post-acquisition.

That is not something a CPA inspired valuation, or a generalized valuation model can give you.

So, the lesson here is to understand that general valuation models can place a value on your business based on profits, quality of management, and comparable deals but that may have nothing to do with how an acquirer with most to gain will think about value.

The secret to creating an unreasonably large $ liquidity event is to build a business through the lens of a buyer. Build a business that passes the Saleability Test. Build a business that buyers love to buy even if you keep it. However, if you build it with an eye to how a buyer thinks, you build yourself an Option Strategy. The option to sell. And if you do sell the following might be true:

The perceived value placed on your business by the right acquirer may well exceed your aspiration on price!

Reach out with thoughts Ian@TPPBoston.com

About the Author

A serial entrepreneur, Ian, has been successfully scaling businesses around the globe for over 40 years both organically and by acquisition. He has established himself as an astute thought leader on acquiring private companies and has completed over 40 deals with an enterprise value of $1B. Ian is a multi-company operator and an investment banker; a rare combination. The C-suite circuit gravitates towards his ability to simplify the complex. Ian has held several leadership roles at public companies: Thomson Reuters, Capita and Mycronic plus several market leading private companies. Most recently, Ian advises CEOs on building businesses buyers love to buy within his company, The Portfolio Partnership. Ian has penned many award-winning books including Fulfilling the Potential of Your Business and The Acquirer’s Playbook, both have been praised as necessary tools for industry leaders as a guide to successful acquisitions.

Our practice does two things well. We build Acquisition Programs into our client’s business alongside their team to create successful serial acquirers. We execute our Value Acceleration System preferably 2 years prior to a desired exit to transform the probability of a remarkable exit. We are operators.

email me